Digital Bonfire … Digital Phoenix?

Monday 17 October 2022 | NewsTech stocks value goes up in smoke – what’s next

It’s familiar territory by now, but it’s truly remarkable to reflect upon the public markets’ decline in tech valuations over the past year (measured by the losses investors have incurred). A little over a year ago, for example, Robinhood Markets listed at $38 and peaked at $55, creating a $48bn market cap company focused on commission-free trading platform for mums and dads. Precisely how it made money with its product was a lot less clear than the money it made for its original investors. Today, the stock is down 80% from its peak.

There are many more examples out there: companies which intended to use a change in consumer or business behaviour enabled by technology to disrupt the status quo and create new propositions, or carve out new niches in existing markets, with rapid growth to reach competitive scale and win market share the key objectives. Building future value with cheap money spent today seemed to be the business strategy for many new-wave disruptor businesses. The last 9 months have seen investors’ faith incinerated on a digital bonfire as confidence has eroded, driven by many such companies missing growth targets or reporting falling customer numbers.

Despite the gloom however, this is not a universal story. Surveying the wreckage, we wondered: what defines a survivor, of this “digital bonfire”? How might a “digital phoenix” rise from the ashes? We’ve looked across the public and private markets, looking for relative outperformers, to understand their stories and to draw implications for value creative action. If you’re curious, read on.

It’s the earnings, stupid

Until recently, growth was the value driver: so spend to grow! Nowadays, if there’s one thing that separates the relative winners from the losers it is profitability and cashflow. Amongst the most prominent, listed tech companies, those that had a negative EBITDA were down 88% vs profitable companies that lost only 40%. Similarly, amongst the technology stocks that IPO’d since January 2021 (105 in total), those with negative EBITDA are down 56%, positive EBITDA but negative Net Income were down still, but only 36% and finally the 11 companies with positive Net Income actually had an average of 4% stock price return.

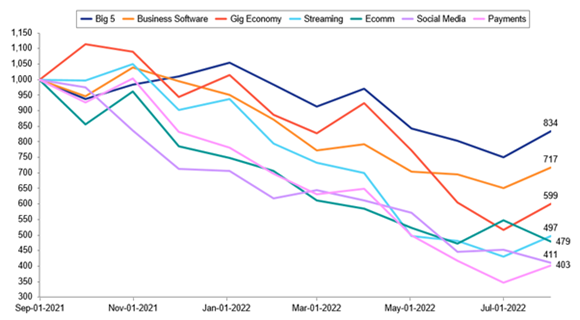

More than just profitability however, it’s the maturity of the business model and the proof points this brings in terms of showing a clear ability to sustain a profit that has protected the best companies from the worst outcomes. The most prominent global tech stocks, the Big Five[1] and established business software players[2] are only down an average of 17% and 28% respectively in the year Sept 2021 to August 2022. Newer players such as gig economy[3], e-commerce[4], social media[5], streaming[6] and payment platforms[7] are down 40-60% on average, very often more individually. The difference? It’s not just tenure (or COVID unwind)… it’s frankly just really obvious how Microsoft makes money, and a lot less obvious how, for example, companies offering grocery delivery on demand can sustainably make money today or even in the future.

So, what to do as a business to regain investor confidence?

Profitability is harder than it sounds to deliver of course, particularly over short time frames. What to do? We think the answer lies in three parts.

Firstly, conserve cash

Where public markets have gone already, private markets are rapidly heading (or have already reached). Either way, conditions for raising cheap equity capital to spend on growth are materially worse than they were a year ago. ”Tech and digital” companies that are not yet profitable need to rapidly focus on eliminating cash outflows that are not directly contributing to sales or near-term capability growth: hiring freezes, reviewing discretionary spend, eliminating questionable marketing spend and so on.

Second, focus, focus, focus: make the hard decisions and prioritise

Now it gets harder, and a lot less obvious. If the key value drivers now are current cashflow and profitability, then the business needs to focus on these. This is uncomfortable for companies focused on future growth and long run unit economics. A shift from activities designed to build long term value to actions that must deliver short term returns will be very counter cultural. To us this means a “focus on the core” but what does this mean? A few thoughts:

1. Core CUSTOMERS: which are the customer segments that are already profitable? Can you focus your marketing spend to find more? Should you invest to retain them? Which segment is the next best prospect for profits? Which segments are marginal and unproven? Can a reduction in customer numbers yield a profitable core?

2. Core PRODUCTS and SERVICES: what is the simplest expression of your product or proposition, that already exists, is easy to describe and takes the least imagination (and fewest leaps of faith) for customers to adopt? What elements of the proposition are core versus less valued by customers? What is the cost of those elements beyond the core?

3. Core CHANNELS: which marketing and distribution channels work today, with known (and measurable) response rates and unit costs? Which are you less certain of?

4. CAPABILITIES and CAPACITY: What capabilities and capacity are needed for a “core” focused business? How much of each is likely to be needed in the next 12 months? How hard are they to reduce and rebuild later? Make the hard decisions now.

5. PRICING and PROMOTION: Are there opportunities to reprice upwards or to reduce discounting? How price sensitive are your core customers? What are competitors doing on pricing?

When you add these together and reflect on the interconnections at work, this amounts to a rapid re-assessment of business strategy but with a focus on re-discovering the core – for customers, for capabilities, for profit and value generation.

Third, think like an investor

We’d encourage investors to consider five things, and managers with them:

1. Get active: If you are insiders push the process of rapid strategic review we have described – force the hard questions to be asked

2. Force a new mindset: Executives need to be held accountable for performance – make responsibilities clear, exercise more direct control, deliver on commitments, hit KPI targets

3. Double down on clarity: If you are looking to invest in “oversold” assets, focus your attention on the business model. Be clear on the path to profit and what the competitive end game is

4. Consider Public to Private moves: Some businesses may need restructuring and then further investment away from the limelight of the public markets before they are ready to come to market again

5. Ask whether less is more: Assess whether the company has a greater chance of survival and value creation if it scales back and reduces its ambitions for growth for 12 to 24 months while the economic storms abate

This investor perspective is (and not accidentally) also a healthy prescription for managers. More than ever, and particularly in the technology sector, managers need to think and act like investors (as, in many cases they are).

In conclusion

At this point, you may be feeling that our prescription – conserving cash, refocusing and thinking like an investor – sounds rather obvious. Surprisingly perhaps, while we see quite a number of companies conserving cash with hiring freezes and the like, we see less evidence of them recognising the likelihood of a sustained period of severe, public questioning. Robinhood is closing offices and has announced two separate restructurings, mostly focusing on reducing operational and marketing staff. It’s difficult to see evidence of a significant refocus at Robinhood however, as it continues to release new, crypto-oriented products and services. What you are doing, and the rationale for it should be made clear, both internally and to investors, particularly in times of uncertainty.

What are you doing? Is it clear to investors? How can we help?

OC&C contacts

_

[1] Apple, Microsoft, Google, Amazon and Facebook

[2] Oracle, Adobe, Salesforce, Intuit and SAP

[3] Uber, DoorDash, Airbnb and Lyft

[4] Alibaba, JD.com, Pinduoduo, MercadoLibre, Coupang, eBay, Shopify and Etsy

[5] Baidu, Twitter, Snap

[6] Disney, Netflix and Spotify

[7] Visa, Mastercard, PayPal, Global Payments, Robinhood and Coinbase

For our analysis, we took a basket of 105 publicly listed stocks in leading economies. We looked at share price movements between 1 September 2021 and 1 August 2022.