The state of travel recovery

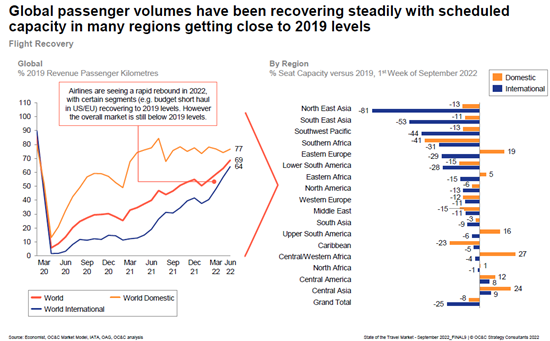

Wednesday, 14 September 2022 | NewsTravel recovery has bounced back quicker than expected, with recovery expanding from strong domestic leisure markets into business and international travel. This level of recovery to date owes credit to the high and effective levels of pent-up demand, especially in the leisure segment where consumer savings were built up and retained during the pandemic. More unexpectedly, business travel has been returning faster than predicted, though the jury is still out on the lasting impact of the pandemic on business travel habits (although remote and hybrid working are clearly here to stay).

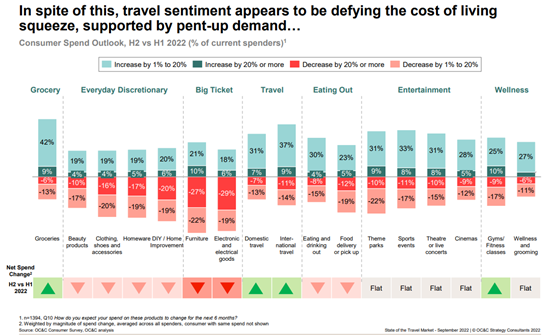

However, the recovery is likely to slow as inflation, labour shortages, and weakening consumer confidence impact the market. Rising fuel costs, wider inflation, labour shortages are all contributing to elevated prices for hospitality, while consumers’ purse strings are tightening. So far, customers appear to be absorbing inflationary impacts and protecting their travel spend, with travel being one of the few areas of spending that consumers expect to increase spending on over the next 6 months.

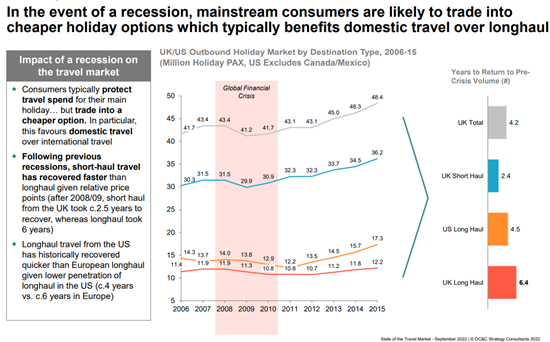

However, as banked savings continue to dissipate, and inflation continues to bite in consumer spending power, this effect is expected to unwind. Consequently, we expect a softening of the recovery through the remainder of 2022. In previous periods of macroeconomic pressure and recession, consumers have traded down into cheaper travel option which has typically favoured domestic travel and other value travel options, with a similar dynamic expected this time as well. Following the 2008-09 recession short haul travel took c.2-3 years to recover to pre-recession levels, with long-haul travel taking c.4-6 years.

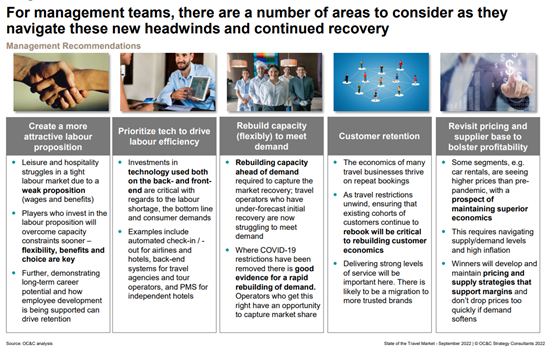

Alongside inflation, the struggle to hire and retain labour is still driving capacity constraints across the industry. To help navigate these trends, management teams need to review their labour proposition, repositioning themselves with attractive flexible packages, and leveraging technology to help drive productivity and bridge any gaps. Furthermore, to drive the recovery travel businesses should look harder at customer reactivation, and also revisit revenue management and pricing strategies to rebuild and sustain profitability.

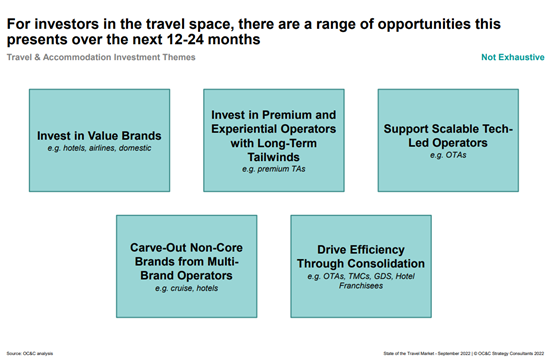

Valuations in public markets softened from highs seen in 2021 with many travel stocks still trading below pre-COVID levels. However, the sector has seen strong levels of M&A with the mix of ‘good’ M&A improving over the last 12 months. For investors who know where to look, there remain attractive opportunities to invest in the sector over the next 12-24 months. For management teams looking to support valuations, the imperative is to demonstrate a recovery to pre-COVID levels alongside a sustainable growth story. We are challenging management teams to think hard about how their equity stories (and KPIs) may need to evolve as we emerge from the Pandemic.

Our latest report on the travel sector, written in conjunction with Harris Williams, outlines the potential shape of the recovery and the implications for investors and management teams. To see more detailed stats behind our findings please click here.