GLP-1s and the Future of Food: New 2026 Insights on Consumption, Premiumization and Market Impact

In 2025, we explored how GLP-1’s were beginning to reshape consumer behavior, identifying early evidence of reduced food consumption and shifting demand patterns. Our latest analysis builds on that foundation, showing that GLP-1s are no longer an emerging disruptor but a structural force in US food and beverage demand.

As outlined in our previous article on the GLP-1 effect on consumption behavior, early adoption was already driving measurable changes in how and what consumers eat. One year on, new data confirms that these shifts are deepening, broadening, and becoming embedded in the market.

GLP-1 penetration is rising – but evolving

GLP-1 adoption continues to expand with active penetration expected to grow from approximately 12% of US adults today to 15–18% by 2031. However, the nature of that growth is changing.

The next wave of users is increasingly weight-focused rather than diabetes-led, marking a fundamental shift in the user base. With this transition comes changing behaviors, expectations, and usage patterns. Notably, weight-focused users are more likely to cycle on and off treatment, contributing to higher levels of churn and “stop-start” usage.

As a result, while the total number of people engaging with GLP-1s will continue to rise, point-in-time active usage will grow more gradually, reflecting this dynamic pattern of adoption.

At the same time, the addressable market remains substantial. Around 14% of US adults are expected to become newly addressable over the next five years, supported by improving affordability, broader insurance coverage, and the introduction of new formats such as oral GLP-1s.

A structural headwind to food and beverage volumes

Our 2025 analysis identified early signs of reduced consumption among GLP-1 users. The latest data confirms that this effect is now material at a market level.

GLP-1s are expected to contribute approximately -0.2% per annum volume drag on US food and beverage demand through 2031. This reflects a consistent pattern: When consumers initiate treatment, they typically reduce portion sizes and eat less frequently, creating a step-change in calorie intake.

While some of this impact is offset over time as users discontinue treatment and consumption rebounds, the overall effect persists due to rising penetration.

From consumption decline to demand reshaping

However, the most important insight is not simply that consumers are eating less, but that demand is being fundamentally reshaped.

GLP-1s are driving three key behavioral shifts:

- More intentional consumption: Users are eating smaller portions, snacking less frequently, and making more deliberate choices about when and what they consume.

- Nutritional prioritization: There is a clear shift toward protein, fiber, and nutrient-dense foods that support satiety and align with health goals.

- Selective indulgence: Rather than eliminating treats, consumers are becoming more selective, focusing on fewer, higher-quality indulgence occasions.

Our 2025 report noted reduced snacking and lower impulse consumption for GLP-1 user’s. Our 2026 data shows that this behavior is now more structured and sustained, reflecting a deeper change in how consumers engage with food.

Category winners and losers are emerging

As these behaviors take hold, category-level impacts are becoming clearer.

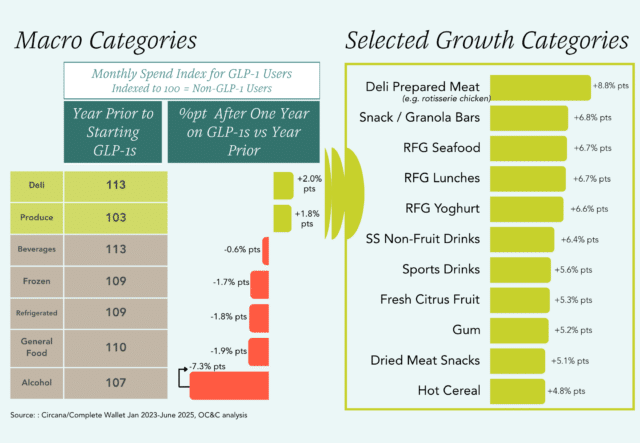

GLP-1 users are shifting spend toward fresher and more functional categories, including protein-rich and ready-to-eat options such as prepared meats, yoghurt, and seafood.

These categories benefit from alignment with dietary guidance around satiety, nutrition, and ease of consumption.

In contrast, indulgent and discretionary categories are seeing the most significant declines. Alcohol, sweet bakery, snacks, and rich or heavy foods are particularly exposed, reflecting reduced tolerance and lower appetite for these products during active use.

Importantly, many of these effects are temporary during active usage, with consumption rebounding after discontinuation. However, there are notable exceptions:

- Alcohol shows a more durable decline

- Produce demonstrates sustained growth

This reinforces the need for a nuanced view of GLP-1 impact, consistent with our earlier conclusion that disruption is uneven across categories.

Premiumization as the economic offset

Despite downward pressure on volumes, overall value impact is more balanced due to a clear shift toward premiumization. GLP-1 users are increasingly opting for higher-quality products, even if they are consuming them less frequently. This reflects a broader reallocation of spend; fewer items per basket, but higher value per item. As a result, GLP-1s should not be viewed as a simple demand destruction story. Instead, they represent a portfolio and occasion reallocation challenge, where value shifts across categories, formats, and price points.

Strategic implications for the industry

The implications for food and beverage companies are significant. First GLP-1s must be treated as a long-term structural factor, not a passing trend. With penetration continuing to rise, their impact will only become more pronounced. Second, success will depend on aligning with the new demand drivers emerging from GLP-1 usage. This includes focusing on:

- Protein density and functional nutrition including Fiber

- Freshness and simplicity

- Portion control and smaller formats

- Reduced sugar and fat intensity

Finally, innovation pipelines will need to evolve toward premium, high-satiety offerings that justify price even as unit volumes decline.

From behavioral shift to structural transformation

Our 2025 analysis highlighted the early behavioral impact of GLP-1s. Our 2026 research shows that those behaviors are now translating into structural market change.

For industry players, the challenge is no longer whether GLP-1s will have an impact, but how quickly they can adapt to a market that is already being reshaped.

How OC&C can Support you

At OC&C Strategy Consultants, we are partnering with clients to navigate this transformation with rigor and foresight. Our team brings unmatched expertise to support your strategic goals, having supported over 500 deals with local players and global champions.

Connect with our industry leaders below or email [email protected] to find out how we can support you.

Suggested articles

View all articles

Friday 8th May 2026

Pockets of Growth in European Beverages: Where Leaders Are Winning in a Low-Growth Market

Across Europe the beverages sector presents a paradox. At a headline level, growth appears modest with per capita consumption has increased only slightly over...

Monday 25th August 2025

Unlocking International growth

Expanding your business through international growth can be a transformational opportunity but also a daunting challenge. While no silver bullet solutions exist, having clear...

Thursday 19th June 2025

Understanding the GLP-1 Effect on Consumption Behavior

GLP-1 medications such as Ozempic and Wegovy, reduce caloric intake by mimicking satiety hormones, slowing gastric emptying, and modulating brain reward signals related to...

Thursday 12th June 2025

The Changing Face of Beauty M&A – How disruption has created a window for new investors

The Beauty & Personal Care (BPC) sector has long delivered strong growth, ahead of the wider CPG landscape. Its combination of emotional engagement, innovation,...

Thursday 22nd May 2025