Calmer Waters Ahead?

Global Travel Outlook

Wednesday 03 April 2024Article

As we emerge from our post-Covid era, travel has walked a turbulent recovery path. Multiple barriers such as high-cost inflation, labour shortages and global conflicts have intersected to create a slow return to normality, both for consumers and operators. However, our joint research partnership with global investment bank and M&A specialist Harris Williams predicts there are calmer waters ahead for the global travel industry, with travel volumes forecast to grow at 4-6% per annum over the next 5 years.

We’ve identified seven critical trends as pivotal drivers of change within the global travel sector:

Resilience of Travel Demand

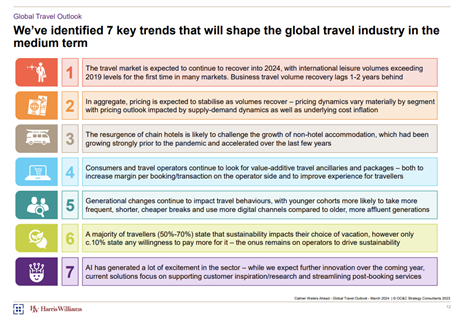

Importantly for operators, consumers are prioritising spending on ‘big ticket leisure’, displaying a willingness to spend Covid savings on travel and related life experiences. 2023 saw global travel prices between 20-40% higher than pre-Covid levels. However, recessions and other anomalies have not impacted travel demand and consumer appetite. Prices are expected to stabilise as volumes recover, with demand strong, and underlying cost inflation set to reduce. A willingness to spend is also reflected in business travel patterns, with global business travel expected to return to or exceed 2019 levels between 2025-2026.

Diverse Travel Preferences Exist Across Generations

Consumer appetite for travel experiences remains strong across generations, with international leisure volumes exceeding 2019 levels for the first time in many markets. Younger cohorts are seeking more frequent, shorter, and lower-cost trips. They are also increasingly utilising generative AI and social media to guide their travel choices and research for the best prices. Older, more affluent generations are happier to invest in longer, more personalised trips. Furthermore, while the majority of travellers are concerned by sustainability, less than 10% are willing to pay more to act on this. Balancing this cost with customer expectations will be key for operators.

The appeal of service bundling

Consumers in general are open to bundling services during their vacations, driven by better prices, a streamlined process, and security measures such as ATOL holiday protection. This trend is beneficial for operators who are able to maximise transaction economics and margin through ancillary sales. Further, the resurgence of chain hotels is likely to challenge the growth of non-hotel accommodation such as hostels and campsites, which typically do not have active relationships with customers.

What are the implications for management teams?

There are 7 critical imperatives for management teams to capitalise on the next wave of travel growth:

- Refine / upgrade commercial strategies to reflect changing demand & yield opportunities

- Maximise customer retention and loyalty

- Strengthen distribution channels beyond paid search

- Seek opportunities to own the end-to-end customer relationship

- Adopt a ‘learn fast’ mindset with technology, including AI

- Refine product & proposition to meet customer needs and maximise value

- Continue to develop leading proposition to talent

What are the implications for investors?

For investors in the travel space, there are a range of potential opportunities that these trends present over the next 12-24 months. Some of these include:

- Ongoing consolidation of corporate Travel Management Companies

- Premium & Experiential Operators with long-term tailwinds

- Inventory-light, digital intermediaries and scalable tech-led operators

- Scalable consumer champion hospitality brands

- Investment across end-to-end value chain with technology, data, and ancillaries

Explore our comprehensive report in collaboration with Harris Williams, delving into global travel trends and their implications for management teams and investors. For further information on our deep expertise contact our Travel Team today.

Jan Bergmann, Partner

Nicholas Farhi, Partner

Phil Hunt, Partner

Simona Dossena, Partner

Tom Gladstone, Partner

Tim Cook, Partner

Mohsin Saleh, Associate Partner

Rebecca Henshaw, Associate Partner

Read Publication